The pay gap is nothing new, unfortunately. We’re all sick of hearing the same shitty excuses from employers to explain bullshit systemic biases, outdated gender roles meaning unequal caring responsibilities and the inevitable motherhood penalty that so many women face sooner or later.

This was put simply by Sarah Coles, Head of Personal Finance at AJ Bell and Headline Money’s reigning Expert of the Year.

She says: “Pretty much when you pay into your pension at work, it’s a percentage of your pay. So naturally, the higher your pay, the bigger the percentage. The gender pension gap comes from the fact that women have lower pay to start with. That’s the root.”

Coles has spent nearly twenty years explaining what’s actually happening to your money, first as a journalist for Bloomberg and Moneywise, then as Head of Personal Finance at Hargreaves Lansdown, and now in the same role at one of the UK’s largest investment platforms.

Her team’s latest research, the AJ Bell Money Matters Gender Pension Gap Report, lays out in numbers what most working women already half-know in their gut: women hold 48% less in their pensions than men, and the divergence starts earlier, and at a more specific age, than almost anyone realises.

The gender pension gap is far more slept on than the gender pay gap, and women who are painfully aware of it often seem resigned to the idea of ending up with a significantly smaller retirement pot than most men.

But there is actually a lot more contributing to this chasm in savings than just the difference in earnings that get continuously compounded over the course of our working lives.

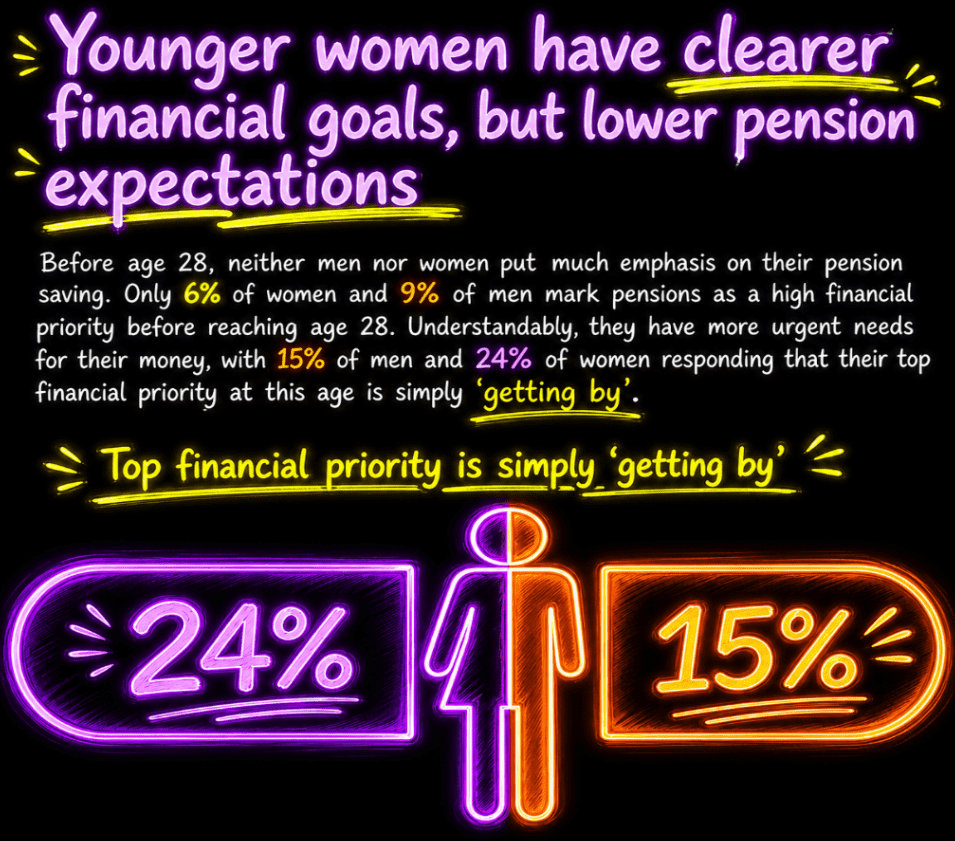

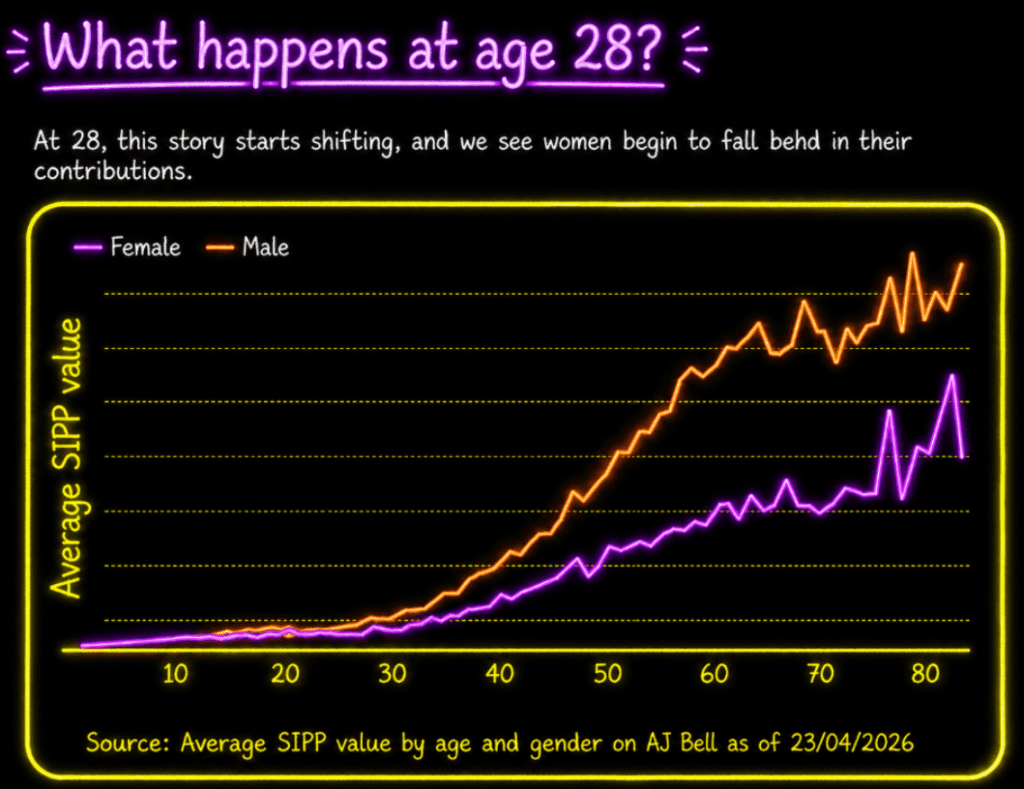

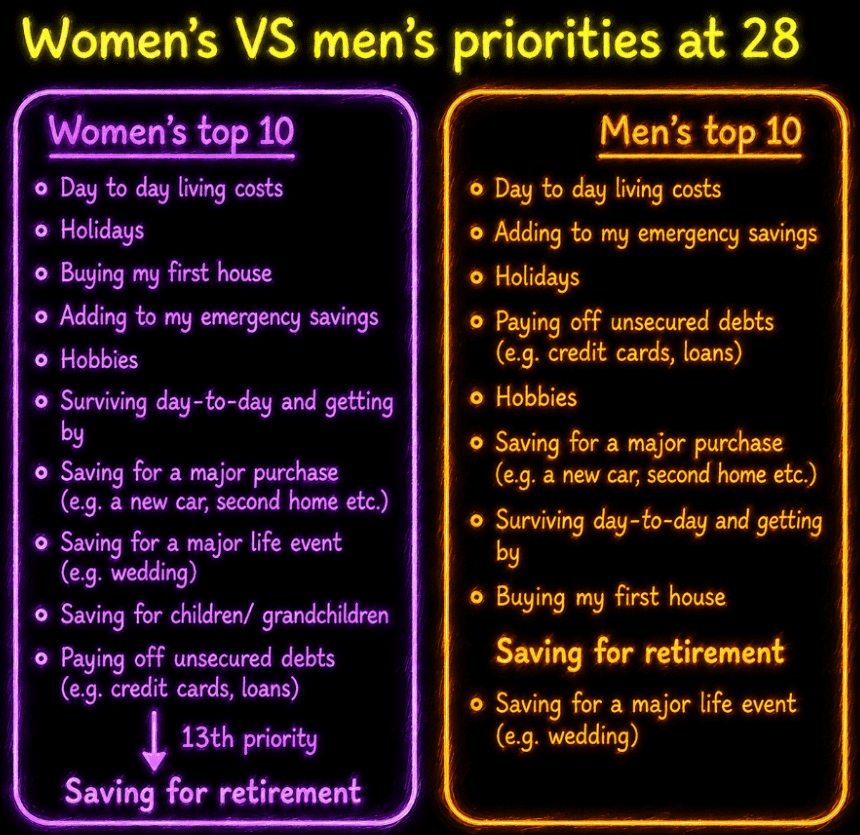

AJ Bell’s own customer data pinpoints the moment of divergence. Among their SIPP customers, men and women’s pension contributions begin to split at exactly 28.

Coles says: “Age 28 is when the gap starts to open in terms of how much people have in their AJ Bell pensions. We asked about priorities, and men are much more likely to prioritise their pension than women at the age of 28. Women are more likely to prioritise saving for a family, just getting by, day-to-day savings, all those other things.

‘’Some of that is gendered, and some of it is to do with purely being on a lower income and having less to go around. For example, you can’t prioritise your income on pensions if you’ve spent it all on heating your house.”

Coles says: “Age 28 is when the gap starts to open in terms of how much people have in their AJ Bell pensions. We asked about priorities, and men are much more likely to prioritise their pension than women at the age of 28. Women are more likely to prioritise saving for a family, just getting by, day-to-day savings, all those other things.

‘’Some of that is gendered, and some of it is to do with purely being on a lower income and having less to go around. For example, you can’t prioritise your income on pensions if you’ve spent it all on heating your house.”

Prioritising family life also directly contributes to the gender pay gap, as Coles explained.

She says: “The Office for National Statistics looked at the jobs and commutes that women and men will do, and they found that women are more likely than men to accept lower pay in favour of a shorter commute. That’s a very clear indication of women compromising for flexibility, because they’ve got to get to school and back, and someone has to be there.

‘’If they’re not paying for childcare, then often one of the couples will have to compromise.”

This of course is not a legal pay gap, but it certainly fucking acts like one.

And it doesn’t stop with childcare. Coles describes what she calls the caring sequence.

She says: “Once you get to 50, you start to see women dropping out of the workforce, and a lot of that has to do with care for old people. Some of it’s cultural that the daughter does the looking after, or the daughter-in-law.

“Some of it is maths- the male partner may well say, ‘I’m earning much more than you, you should be the one to stop work.’

“We see a lot of women dropping out of the workforce at that point. You care for your kids, then you care for your parents, then you care for your partner.”

What a terrifying prospect.

Another important note is that although Ctrl+Shift will always support the independence of our readers, it can actually be counterproductive to do this with household finances, Coles advised.

She says: “Couples who have been completely independent in terms of their money will consider themselves to be completely independent when they have kids. When one of them has worked part-time and had a massive pay cut, you’ve got somebody who is trying to act like an independent person within a couple, who just has less money to go around.

“This leads them to think to that they can’t afford to pay into their pension.’’

Coles suggests that dialogue about managing pensions is just as important as managing a mortgage:

“When a woman goes on maternity leave, couples will sit down and go, ‘How are we going to pay the mortgage?’ There’s no reason why you can’t do that with your pension as well.”

For all readers who are long term relationships and feeling ready to settle down and live happily ever after, please take notes:

Coles says: “Even if you’ve got a great relationship and you’ve completely worked out how to do everything, and you retire and you’ve both got this income together, you are going to have disagreements over how to spend that money. And if you have no or a much smaller pension, you’re going to have much less of a say.

“If your partner says, ‘No, you’re absolutely not going to spend your money on this,’ you can’t say, ‘Don’t worry, I’ll just spend my money,’ because you haven’t got any. So you lose your agency.”

Economic inequality affects our freedom even in old age. That’s got to be the most infuriating fucking thing you’ve heard all day.

And not to the pile on the doom and gloom but things don’t get much better for divorcees, according to Coles.

She says: “In divorce, what tends to happen is often people just won’t consider the pension at all, which is terrifying, because it can be worth as much as your house, yet you’re arguing over the house and just going, ‘Yeah, you look after your own pension.”

“Also, if the mother prioritises staying in the house with her children, she will likely offset the pension against the house. This means giving up all of the husband’s pension in order to keep the house. But then of course, they have to start their pension from scratch”.

That is quite enough bad news for now, thanks Coles. Not ideal but better the devil you know, I suppose.

The good news is that there are pension related opportunities that are already on the table. The issue is that women are often simply leaving them there.

When asked what the first piece of actionable advice she would give to women would be regarding pensions, Coles said:

“When you’re coming up to maternity leave, it’s really unsurprising that a lot of people will think, ‘I can’t really afford to keep paying into my pension,’ and they’ll stop their contributions. Or, even if you keep paying into your pension, let’s say you’re paying 4% of your salary, so during maternity you’re paying 4% of your maternity leave salary which it’s a much smaller sum of money from you going in.

“However, your employer will still be paying 4% of your full salary. So if you can spare that money, it gets supercharged by your employer. “

She added that the deal gets even better for women on what’s called a salary sacrifice arrangement, a tax-efficient way of paying into a pension that’s taken from your salary before tax. In many cases, the employer ends up covering the contribution entirely during maternity leave.

“So don’t assume that when you go on maternity leave that you should stop,” Coles says. “Look at what your employer will offer you.”

The second move costs nothing and works in your sleep: set your contribution as a percentage of your salary, not a fixed amount. Every raise lifts the contribution before you’ve had a chance to spend the difference.

Coles says: “It’s really easy to let lifestyle creep take over, where you gradually get a slightly better version of something. Setting a percentage means every time you get a pay rise, you automatically put more into your pension. You’re not having to commit more now, but you’ll make sure you’re committing more every time you get a pay rise, before you’ve had a chance to spend the money on something else.”

“People sometimes assume they will earn a rising trajectory throughout their career, whereas people’s incomes peak in their 40s. There’s a lot of people working shorter hours or having to make compromises around care,” Coles says. “There’s a whole heap of things that can happen later in your career. Instead of thinking it’s definitely going to go like that, you really need to think about the different factors in your life that could mean you earn less when you get older.”

When it comes to managing pensions in relationships it may seem trivial, but Coles encourages open discussion regardless.

She says: “I think the conversation is the important bit. Just talk about the impact of it all the way through.

“An important question to ask your partner if they earn more than you is ‘If l have a smaller pension later, I will need to live off your pension. Are you happy with that?’. You’re not saying, ‘Give me all your money now.’ You are saying, ‘I’m making sacrifices in my life. What sacrifices would you like to make in yours?’

“It’s really important to understand the approach to money of your partner. If you’ve got a partner who’s going to struggle to spend money in retirement, and you really want to spend money in retirement and go on holidays, you need to factor in the fact that if you haven’t got money in your own right, that’s going to be a big struggle for the whole of the rest of your life.”

For anyone who’s lucky enough to have a partner that supports them financially even when they’re working, it’s worth noting the higher-earning partner can pay into the lower-earner’s pension directly.

Coles says: “If you’re not working and your partner is, they can put £2,880 a year into your pension, which will get topped up by tax relief, even though when you’re not working you’re not paying any tax. So £3,600 will go into your pension every year.

“It’s perfectly possible to top up someone else’s pension and to make sure that they’re building for the future.”

That is just one great example of the redressing of the balance that is needed to tackle the gender pension gap, but it’s a fucking joke that women have to learn every possible loopwhole just to strive for parity in their pensions.

Coles presses on with a burnout related piece of advice:

“If you’re worried about burnout, one of the things people might feel is that they’re locked into work for longer because they don’t have enough pension and they’ve got to keep flogging themselves stupid. So it’s worth doing the maths with an online pension calculator to work out how many more years you’ll have to work for.

“If the answer is that you will be, say 95, you might not mind living off the state pension.

“People might be able to retire earlier than they thought they could and it gives people a bit of hope that actually they can retire and belief that this date when this hard work can end is going to come at some point.”

That’s the lighter note we were waiting for Coles.

She ties up her words of wisdom with a call to action to all women:

“Not naturally, but culturally, there’s an expectation of women that they have to know an awful lot about something before they consider themselves to know enough. You might find women know everything they need to know about pensions, but they just don’t feel that they’ve got it.

“They think there must be a secret out there that they just don’t know. You don’t have to be ready to sit A level in it. You just need to know enough and then get started. Read one thing, watch one video, use one calculator. Phase it in slowly. You don’t need to know everything today.

“If you’ve left it late, don’t be so disheartened by the gap that you’ve got to make up that you put it off. You don’t know what will happen in your life. You might inherit something. You might get a lump sum of 10 grand and put that straight in your pension. Whenever we think we’re going to fail, it’s very tempting not to try. Just don’t assume you’re going to fail. Make a start.”

The pension game is shockingly unfair but there are certainly ways to even up the odds a little. From relationship advice to making the most of our employers, hopefully this piece has offered some reassurance.

And lastly. Truly. Fuck the gender pay gap.